News - Moody's Keeps Unibank Ratings Unchanged with Stable Outlook

Business Strategy

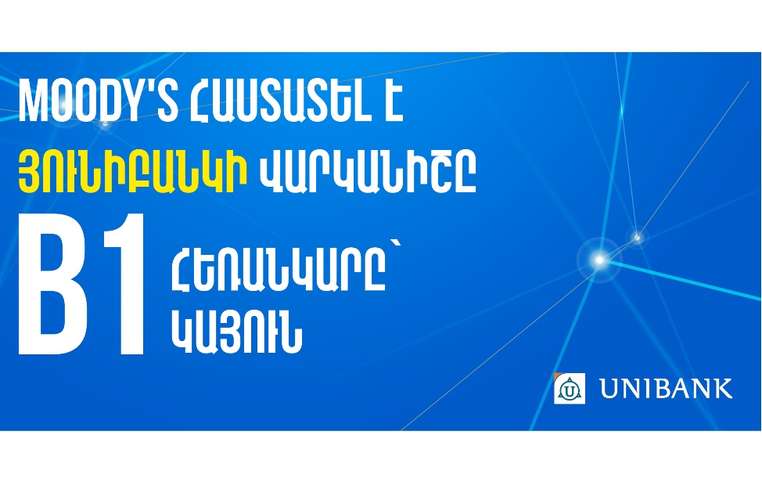

Moody's Keeps Unibank Ratings Unchanged with Stable Outlook

In a recent announcement, Moody's Ratings reaffirmed Unibank's long-term deposit ratings in both national and foreign currencies at a B1 level, maintaining a stable outlook. The agency also confirmed the bank's baseline credit assessment (BCA) and adjusted BCA at b2. Additionally, Unibank's short-term deposit ratings were sustained at NP, with counterparty risk ratings (CRRs) assessed at B1/NP and counterparty risk assessments (CR Assessments) remaining steady at B1(cr)/NP(cr). This reinforcement of ratings comes on the heels of notable improvements in Unibank's asset quality and continued robustness in profitability levels, coupled with a reduced dependency on market-driven funding sources. The enduring confirmation by Moody's underscores Unibank's fortified asset management strategies, as well as its adept handling of financial conditions that uphold its creditworthiness. These ratings, positioned at the B1 level, signify a moderate level of risk, reflecting Unibank's conscientious performance in stabilizing and optimizing its operational frameworks. The consistent ratings and stable projection suggest a positive future outlook, indicating that despite potential economic fluctuations, Unibank remains resilient. Investors and stakeholders can interpret these affirmations as positive indicators of Unibank's fiscal health, reflecting its capacity to sustain healthy financial operations amidst a varying economic landscape. Furthermore, the process of rating reassessment underlines the comprehensive analysis undertaken by Moody's to evaluate the bank's credit metrics, strategic initiatives, and its overall alignment with the financial environment. As the banking and economic sectors adapt to global changes, Unibank continues to present a model of financial equilibrium supported by efficacious governance structures and market strategies.

About usyoo

Categories

Tags